- Fink 🧠

- Posts

- 🔔 Abandon Hope All Ye Who Enter Here

🔔 Abandon Hope All Ye Who Enter Here

The title's pretty bleak, but this isn't about the overwhelming sense of hopelessness as we drift helplessly towards economic oblivion. We're better than that.

However, if you think anything that happened in the UK this week is about central banks pivoting from all the hawkishness, I will be the one to unapologetically piss on your chips.

They aren't pivoting. The Bank of England intervened because pension funds got caught with their pants down (again) and were leveraged to the tits in illiquid markets (again). This doesn't mean the return to QE Infinity.

Let's quickly explain what happened and get it out of the way. Kwarteng's budget announcement was the spark for the UK bond selloff, but that quickly turned into a raging, fiery doomloop of margin calls > bond selling > more margin calls.

The BoE had to step in temporarily as a market-maker of last resort to stop the disorderly selling from spiralling further.

It's not QE all over again. Nevertheless, it IS a SLIGHT shift in the probabilities.

The more of these incidents in global financial markets (and there will be others, because higher rates are to hidden leverage what Sherlock Holmes is to mysteries), the more markets will begin to price the big pivot back to rate cuts.

This is an excellent read if you want more detail 👇

There's a non-paywall, less technical version here or the REALLY basic version here 👇

It's always the same

1. Erroneous assumption of safety

2. Leverage up (key)

3. Ignore warning signs because it's 'safe' (or the positions are too big to exit anyway)

4. Ring up the central bank and bitch about the market disorder your margin call creates

5. Blame someone else— Tim (@VolaTim) September 29, 2022

Moving on...

By now everyone knows we're heading towards recession. The questions are how long until it hits, how bad it'll be, and how long will it last?

Put another way... Where are we in the cycle?

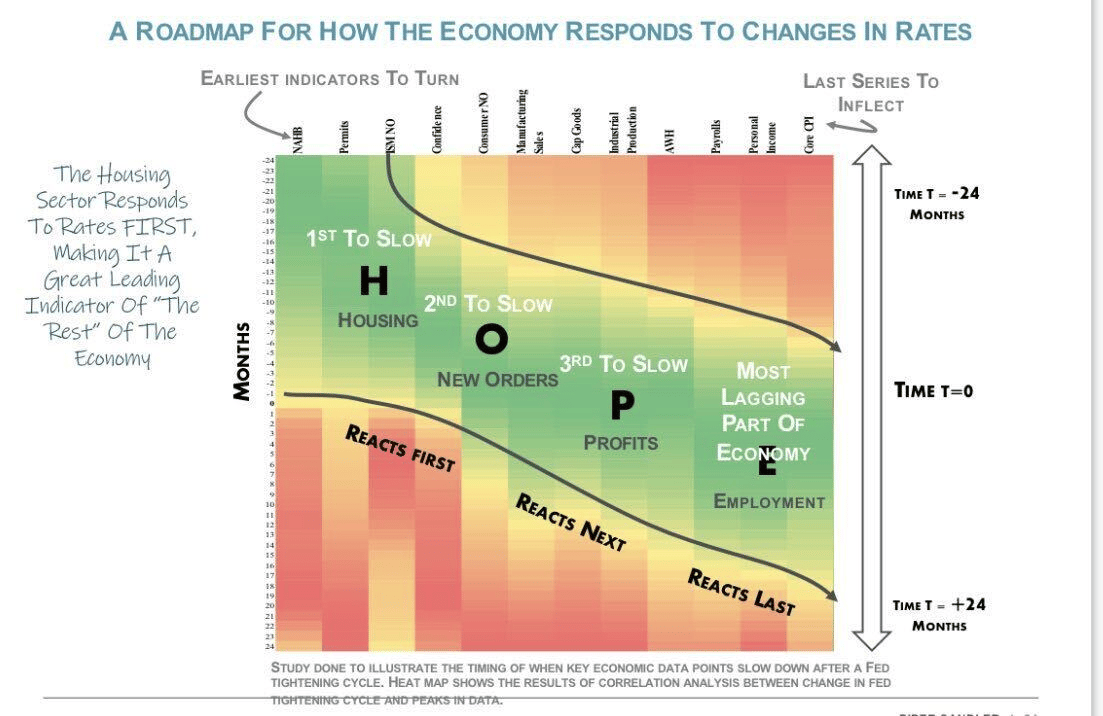

HOPE Springs Eternal

You may have seen this before. It's a great roadmap for how the economy responds to rate hikes. Usually this plays out over a period of approximately two years 👇

Michael Kantro

First, Housing slows, then new Orders, followed by business Profits, and finally Employment: HOPE.

The time element is probably the least important. Things change at different speeds, the data's all over the place due to Covid disruptions, and central banks are all aboard the Rate Hike Express.

The Plan

So, Housing.

We've got 7% mortgage rates in the US, the UK no longer has a mortgage market. The RBA's arsecheeks are clapping andthey're already talking publicly about the risk of rate hikes hurting the housing market (my preciousssss).

Basically, we can all agree that the housing markets are basically frozen. Let's not get carried away, this doesn't mean an imminent plunge in housing prices. Adjustment takes time. It likely means fewer transactions, and a bad time to be an estate agent.

ING has a great explainer: US housing recession is already here

A housing market downturn will weaken the US growth story, but it is also important to remember it will dampen inflation too. Shelter is the largest component of CPI with a one-third weighting via the primary and owners’ equivalent rent components. As the chart shows there is a lag of 12-16 months between movements in house prices and the shelter components of CPI – rents are typically only changed once a month is one reason.

It suggests we may be soon getting to a turning point in the annual rate of change in these key CPI rent components, which if so, can meaningfully depress consumer price inflation through 2023 and likely contribute to getting the US inflation rate back towards 2% by the end of 2023. While the Federal Reserve is downplaying the possibility, we are firmly of the view that interest rate cuts will be on the table in the second half of 2023.

So, let's say that Housing is old news now. The worm has turned and it's all downhill from here.

How about those new Orders? We covered this in detail for Capital here 👇

Clue's in the title. Demand is tanking, and we can add another plunge in container rates (-28% in 3 weeks) to the picture...

📉 And down ANOTHER 10% this week

28% in 3 weeks 🤮 https://t.co/1WVvwDOejm— Tim (@VolaTim) September 29, 2022

In the US, inventories are rising as sales growth slows...

pic.twitter.com/7a0VSyxw78— Kathy Jones (@KathyJones) September 28, 2022

As demand slows, businesses will focus on clearing stock, often at a discount.

So, the Orders slowdown can be checked off too. Both the H and the O are firmly underway and pretty entrenched dynamics.

Which leads us onto Profits...

The profit squeeze is starting, but it's not everywhere yet...

Two stories from the UK today 👇

Next cuts sales and profit guidance as it eyes 'uncertain' winter ahead https://t.co/McoRXF7Bal— Sky News (@SkyNews) September 29, 2022

And this is perhaps the biggest market risk. Everyone supposedly knows that a lot of the forward earnings estimates are <ahem> somewhat optimistic, but it seems they're not priced in yet... 👇

MS (Wilson) - $FDX illustrated how big earnings disappointments are not priced, leaving Fire and Ice in full gear. Strong $USD is yet one more reason for concern on the earnings front. pic.twitter.com/MrMOLsTN2I— †DoejiStar⸸ (@DoejiStar) September 27, 2022

Apple was also punished yesterday after rumours of iPhone production cuts and slowing demand hit the wires... 👇

Now there's something you don't see everyday. A rare red day for AAPL in a sea of green. Can't help but notice how heavily it stands out. pic.twitter.com/sNlttENj63— BlackHeartRedSpade (@bheartrspade) September 28, 2022

Profits are really the big focus now. However, it might require a bit more digging than usual... Gavekal highlight the tendency for companies to get their creative juices flowing when things start to look bad 👇

Here’s the logic: As business conditions worsen, big publicly traded companies find it harder to generate profits that would please Wall Street. So their accountants come to the rescue. But accounting magic has its limits, so their earnings inevitably drop, causing the two data series to converge again.

Simple enough. They'll hide it until it can't be hidden any more...

But the CEO's are a bunch of blabbermouths and undermine the accountants hard work anyway 👇

CEO confidence has deteriorated, which doesn’t bode well for corporate profits.

Source: @Lvieweconomics pic.twitter.com/F2UCTaM7i1— (((The Daily Shot))) (@SoberLook) September 29, 2022

Last, but definitely not least... Employment. The last resort. When companies are forced to cut costs, (what else can you do if demand is anaemic and profits are pressured) they eventually get around to laying people off.

We've already seen plenty of companies announce hiring freezes, but that just means they're not adding to the roster.

There's also been a few layoff announcements, especially in tech, but people are still finding work, which is why Powell highlighted the Vacancies/Unemployment ratio and quits rate (JOLTS survey) as a key metric for the Fed to determine labour market tightness.

They're laser-focused on these factors, because job-switchers have (especially) been able to command big wage increases. 👇

The Fed wants to break this powerful employee dynamic. But how long will that take?

It looks increasingly as if we're moving into the P section, which (if the 24 months is a guide) suggests another 12 months(ish) before the process of economic destruction ends.

I can't end this on such a depressing note. So here's a picture.

I regret nothing.