- Fink 🧠

- Posts

- 🔔 The Infinite Bull Market

🔔 The Infinite Bull Market

"Hey, I'm new here, going to be trading equity indices. What's the best strategy?"

"Just BTFD and leave me alone noob"

So, is long only the way to go?

Let's take a look at the historical returns using this excellent timeline from Goldman Sachs

PiQ

It's clear that being long has yielded far better returns than being short...

"So, you're serious about just BTFD... Surely it can't be that easy?"

Not saying anyone should just blindly buy every dip, this isn't financial advice, DYOR, trade your own strategy etc. but those numbers can't be ignored...

Bull Cycle Average +143%

Bull Cycle Average Time 4.2 Years

Bear Cycle Average -35%

Bear Cycle Average Time 1.6 Years

On average, bull cycle returns are four times larger than bear cycle returns, while bull cycles last 2.6 years (31 months) longer than bear cycles.

So, higher average returns AND a longer average cycle

Averages don't show everything though... 👇

On top of that, stock indices are designed to ditch the worst companies and incorporate the best. Natural selection is built into an index.

What else is notable?

Check out the most extreme returns in the bull cycles (L-R)

369%

308%

150%

254%

220%

302%

101%

401%

Not shown: 116% (so far) since the 2020 Covid lows

20 cycles across the past 121 years & the post-Covid rally is only the eighth largest...

The rally has been FAST and attracted a lot of inflows...

The hunt for yield is at the heart of this.

Capital must be deployed, returns must be generated.

And with government/corporate bond yields historically low, they're simply not attractive assets to hold. 👇

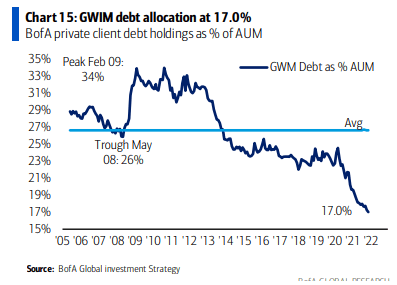

Which means pension funds are being forced to move further out on the risk curve, away from traditionally safer investments and into 'alternative assets'...

U.S. pensions are hundreds of billions of dollars short of what they expect to need to pay public worker retirement benefits

~WSJ

Consider the implications of this 👇 (emphasis added)

The board of the nation’s largest pension fund voted Monday to use borrowed money and alternative assets to meet its investment-return target, even after lowering that target just a few months ago.

The move by the $495 billion California Public Employees’ Retirement System reflects the dimming prospects for safe publicly traded investments by households and institutions alike and sets a tone for increased risk-taking by pension funds around the country.

Without changes, Calpers said its current asset mix would produce 20-year returns of 6.2%, short of both the 7% target the fund started 2021 with and the 6.8% target implemented over the summer.

The trustees also voted to increase riskier alternative investments, raising private-equity holdings to 13% from 8% and adding a 5% allocation to private debt.

Calpers’ investment office already had authority to use leverage—up to 20% of the fund’s total value—as part of investing decisions. But Monday’s decision marks the first time the Calpers board has made leverage an integral part of its asset mix, building it into the fund’s plan for meeting its investment-return target.

Fund staff said they might want to use borrowing that way more going forward.

This illustrates the problem for pension funds such as the $495 billion California Public Employees’ Retirement System 👇

Source

To top it off, they're even competing with central banks for risk exposure 👇

@VolaTim

The Swiss Central Bank is LITERALLY printing money & using it to buy foreign stocks!

See, low interest rates create a positive feedback loop that's best understood visually...

This graphic from Corey Hoffstein/Newfound Research lays out the incentive loop beautifully 👇

If we accept that The TINA* Effect is a powerful driver of US stock markets, and we look at the historical evidence, it's hard to ever make the case for being short (unless the dynamics change)...

Therefore...?

INFINITE BULL MARKET 🚀🚀🚀

*There Is No Alternative

All well and good, until a shock event means that everyone is forced to sell at the same time... 👇

Liquidity Cascades

Click the link to read the full paper (it's free) 👆

And the role of liquidity is so important to understand.

From the paper:

Regardless of cause, a feature of current markets is a dramatic mismatch in liquidity needed versus liquidity available during periods of market stress.

This leads to a structural imbalance when it is met with the systematic, and often convex, hedging pressures of option markets, levered and inverse ETPs, and more.

These imbalances can lead to liquidity cascades, as the hedgers are liquidity takers during periods of liquidity stress.

Don't know what financial news stories are important and what is complete bullsh*t? Hop onto our filtered news channel.

It's completely free 👇👇👇

And if you really want to get to grips with how global markets and economics work, with trade ideas to give you actionable context, then come and join us as a premium member where you're likely going to get a nice Market IQ boost. 👇

SPECIAL OFFER: Right, so we wanna get more people with us long term.

The simple fact is that providing a monthly subscription means too many who want instant gratification join Macrodesiac. We want you to learn FOREVER for pretty damn cheap... £199 FOREVER, instead of £399. Click here to get on for LIFE now (runs out the end of this week!)

Check out our reviews on TrustPilot 👇👇👇